The Resilience Engine (RE) is an InsurTech marketplace for innovative agricultural and climate risk insurance solutions for smallholder farmers globally. RE provides a complete system that accommodates multiple data sources and a platform for administering insurance and supplying value-added services.

RE is a single aggregated platform that unites industry experts, organizations, and their respective networks. It combines the latest technological know-how with best-in-class market understanding and market access. RE supports roll-out and scale-up of climate and agriculture insurance, enabling smallholders to enjoy more secure livelihoods and greater despite climate change. The platform helps actuaries to create and price new products rapidly. It reduces the cost of managing distribution, products, and processes by more than 40%.

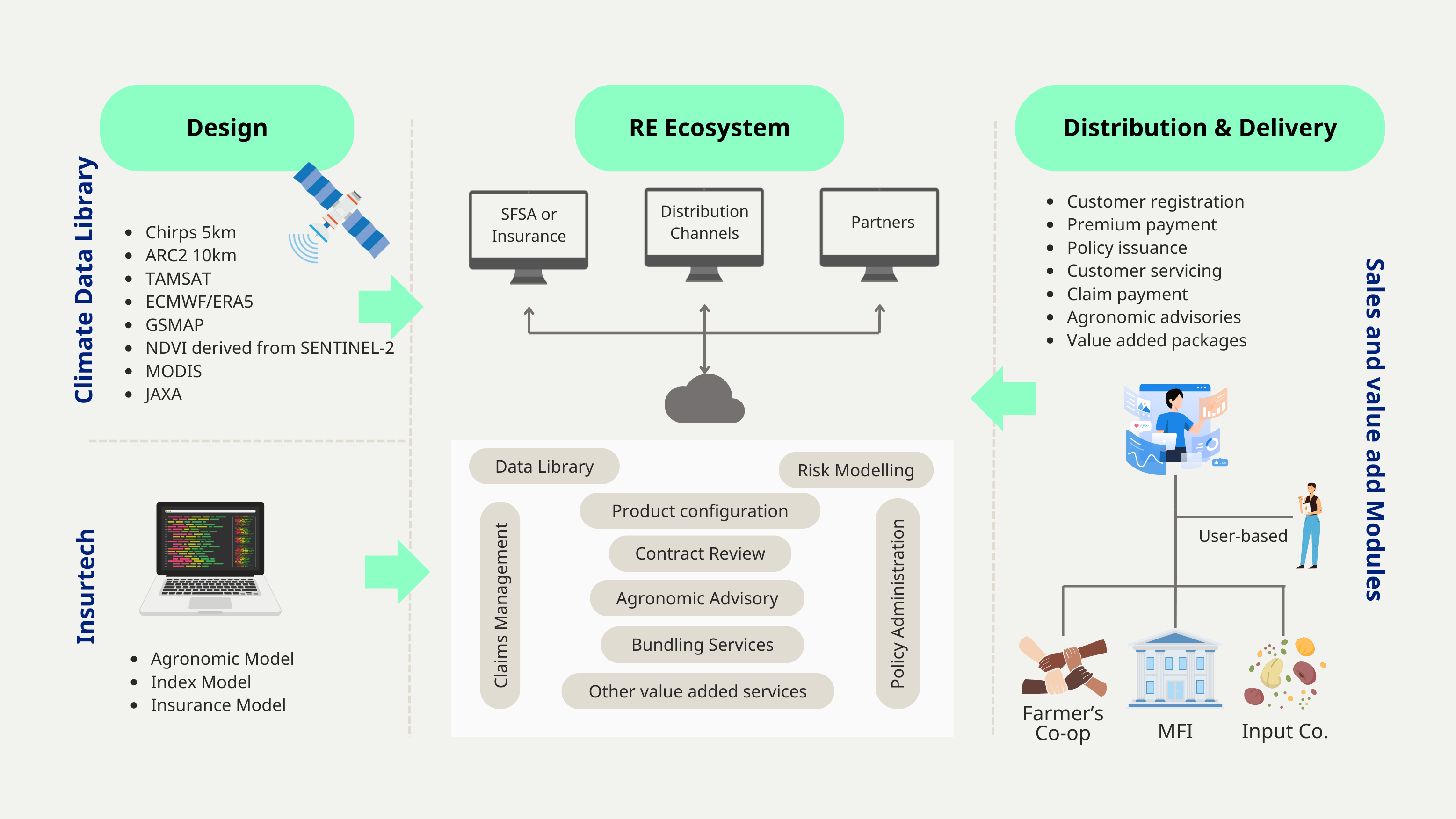

The platform has 6 key modules:

The data library accommodates all satellite and ground station data running online on the RE platform.

Product configuration is where actuaries combine mathematical formulae with agronomic data to design weather index insurance.

A marketplace ecosystem is a sales environment for various channels. Different underwriters can access products independently. Some products are open to all, others are tailored to specific needs.

Customer onboarding: Field data collection uses both digital and traditional tools. Digital tools include mobile apps for customer registration, phone-based USSD technology for onboarding and servicing. Via SMS, farmers can send details to a specific number and the technology can identify their location for registration. Traditional customer onboarding approaches are well integrated with RE; sales teams can upload customer information from an Excel file.

Claim calculation. RE can integrate customer onboarding, satellite data, and product index formulae to calculate claims based on pre-determined triggers.

Agronomic advice. Insured farmers can access digital advisory services delivered through the customer onboarding modules. These services include guidance on-farm management and weather.